Where Will Micron Technology Be in 1 Year? – The Motley Fool

Shares of Micron Technology (MU -1.10%) are down 47% over the past 12 months and the company’s results for the first quarter of fiscal 2023, which were released last week, indicate that things will get worse for the chipmaker before they start looking up later in 2023.

The memory specialist saw a sharp decline in revenue in the most recent quarter, which ended Dec. 1, and slipped to a loss as compared to a profit in the prior-year period. The guidance for the current quarter suggests that rough times are here to stay for a while. However, management anticipates that the memory industry’s fortunes could start turning around in the middle of 2023 as customers start restocking chips.

Let’s take a look at whether Micron will be in a better position a year from now.

Weak memory demand has dented Micron Technology

Micron’s fiscal first-quarter revenue fell a massive 47% year over year to $4.1 billion, driven by a combination of lower memory shipments and a sharp decline in prices. This also led to a big drop in margin. The company’s adjusted gross margin fell to 22.9% from 47% in the prior-year quarter.

Not surprisingly, Micron posted an adjusted loss of $0.04 per share as compared to a profit of $2.16 in the prior-year period. The company’s guidance suggests that things are about to get worse. Management anticipates an adjusted gross margin of just 8.5% this quarter, down nearly 40 percentage points as compared to the year-ago period. The company has guided for an adjusted loss of $0.62 per share versus a profit of $2.14 per share in the prior-year period.

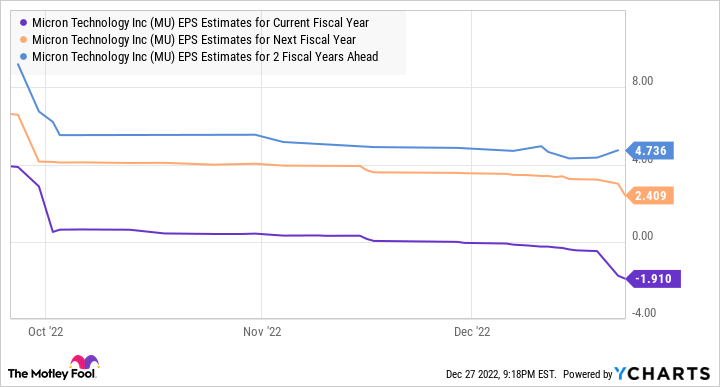

Analysts aren’t hopeful of a turnaround in the full fiscal year, forecasting a 42% drop in revenue to $17.9 billion and an adjusted loss of $0.10 per share as compared to last fiscal year’s earnings of $8.35 per share.

This is not surprising as the demand for memory chips has weakened after a drop in personal computer (PC) and smartphone sales.

And the demand for memory chips deployed in servers and graphics cards has also slowed. All of this has created an oversupply of memory chips. As a result, the price of dynamic random access memory (DRAM) chips is expected to decline between 13% and 18% in the current quarter, worse than the 10% to 15% decline seen in the third quarter.

This explains Micron’s woeful guidance. But at the same time, management did indicate that there could be a turnaround in 2023.

Things turn around in the coming months

CEO Sanjay Mehrotra said on the latest earnings conference call that “customer inventory, which is impacting near-term demand, is expected to continue improving, and we expect most customers to have reduced inventory to relatively healthy levels by mid-calendar 2023. Consequently, we expect the fiscal second-half revenue to improve versus the first half of our fiscal year.”

But Mehrotra did add that profitability could “remain challenged through calendar 2023.” But investors can expect an improvement in demand for memory chips to lead to better margins as companies operating in this space are cutting investments and pulling back production amid the weak demand.

Micron’s forecast about a turnaround in memory demand is in line with other, third-party forecasts. So things might start looking up for Micron in the second half of 2023 as demand for memory chips comes back, but it may take some time before the demand/supply balance is restored and prices start heading higher.

Specifically, DRAM bit demand is expected to increase only 8.3% in 2023, which would be the first sub-10% increase in history. Throw in production cuts by the likes of Micron, which is reducing output by as much as 20%, and the memory industry could be close to achieving a demand/supply balance.

But Micron probably won’t regain its mojo until 2024. PC sales are expected to rebound in 2024, while smartphone sales are expected to gather momentum starting from the second half of 2023. As demand begins to pick up and supply is tightened, the steep price declines that the memory industry is witnessing should diminish.

As a result, Micron is expected to turn in a highly improved performance in fiscal 2024 (which will begin in September 2023). Analysts are forecasting a 42% increase in revenue and a return to profitability in fiscal 2024, followed by another solid year in fiscal 2025.

MU EPS estimates for current fiscal year; data by YCharts.

So Micron Technology could be in a much stronger position after one year, though a couple of important things will have to fall into place for that to happen: an improvement in demand and tight supply.

Investors would do well to keep an eye on a potential turnaround and keep this tech stock on their watch lists in 2023, since it has a history of performing well during a memory boom cycle.