Meta Materials: Disruptive Technology, But Poor Fundamentals … – Seeking Alpha

PhonlamaiPhoto

Meta Materials Inc. (NASDAQ:MMAT) studies, develops, and produces disruptive metamaterials that can be used in the most disparate ways and in different industrial sectors. From augmented reality to autonomous vehicle driving, lithium battery safety, and much more. The uses are really interesting and allow us to solve real and highly topical problems. The underlying market is growing rapidly (expected double-digit growth) and this represents an important opportunity for business sustainability.

If we look at the revenue growth we can see how the applications developed (above all in the holographic sector) are producing respectable results. Revenue has gone from $1.1M to $11.1M in two years and this is a positive element but if we look at the constituent elements of revenue we can underline how these make the growth unstable in the next quarters. High operating expenses and the need to find new capital to finance growth over the next 12 months represent an additional element of risk.

A large contract signed with a leading company in the production of lithium batteries could mark the company’s flight. At the moment the risks related to the business represent a high probability of failure and I prefer to wait for new confirmations before opening any long position. My rate is Hold.

Company overview

Meta Materials Inc. studies, designs, and produces highly technological materials used in the most varied ways and different fields of application.

The three core sectors are holography, lithography, and wireless sensing.

Holography is known as the feature that can create three-dimensional images of all sizes. With this production technique, the company can solve counterfeiting problems related to banknotes and credit cards (where three-dimensional images are printed)

The lithographic technique is used to produce films capable of absorbing and/or treating energy sources. It can be used in semiconductors, in phone or car batteries (to increase performance), but also on the house’s windows (to improve the 5G signal).

Finally, the wireless technology designed by Meta Materials makes it possible to modify electromagnetic waves and improve the performance of, for example, medical devices.

Meta also uses AI-based software to design and implement its products/services. According to the Company, this represents a competitive advantage as it allows the creation of prototypes faster and cheaper than competitors.

The main customers could be found in the energy, aerospace, health, 5G communications, electronics, and automotive industries.

Highlights and why to buy

Electric Vehicles are the big trend

EV units are expected to grow two-digit or by 22% in the next two years. On the other side, the demand for lithium-ion batteries used in electric vehicles is expected . The main manufacturers are focused to utilize safer and faster and cheapest batteries on vehicles. This represents a very big opportunity for suppliers like MMAT.

MMAT Investor Presentation Nov 2022

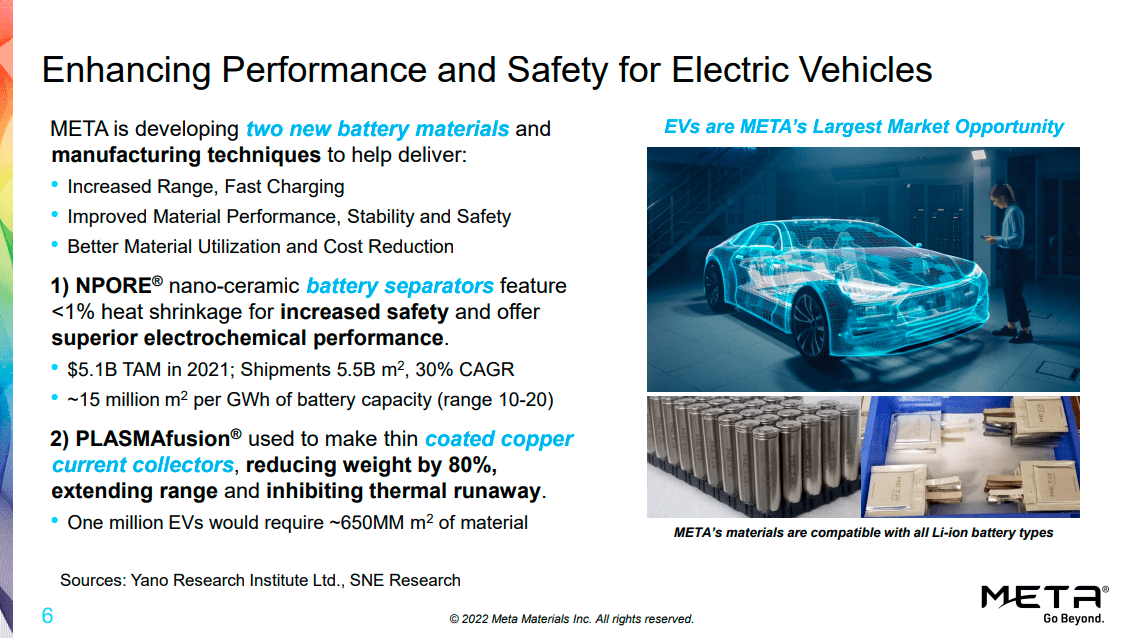

One of the most important aspects of the battery manufacturer is the safety related to the possibility of overheating the battery elements until they cause fire or explosion. This is mainly due to the increased stress to which the batteries are subjected due to the need to recharge them faster.

MMAT is on the market with two solutions to make the use of lithium batteries more efficient.

The first solution is based on nanopores and is named NPORE. Simplistically, the concept is based on a nano-ceramic film used as a separator for the battery elements. This technology makes it possible to obtain a particularly high degree of safety such as preventing any damage following overheating of the elements. According to the Company’s founder (last earnings call):

Demand is expected to grow at about 30% CAGR. And this translates that with each gigawatt of new battery capacity, you would require about 15 new million square meters of battery separator material.

And, related to the commercial and production point of view:

We are currently in discussions and evaluation with various OEMs and Tier 1 suppliers about NPORE… where we’re going to also outsource some of the coating trials, and this is underway with a partner in the East Coast, who can produce NPORE at very large scales.

It seems that the company is organizing itself for the supply of the product on an industrial basis and has also identified the production plant to meet large-scale demand.

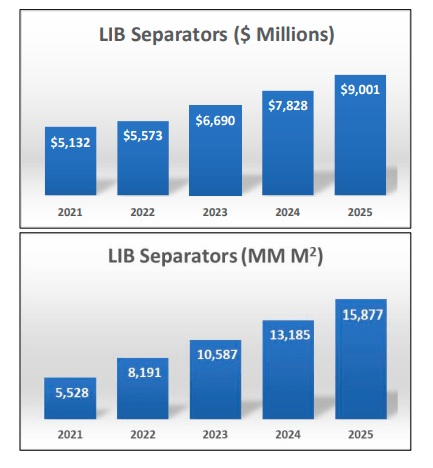

From the demand point of view and , the lithium-ion-battery (LIB) separator market is $5.5 billion in 2022 and it could reach $9 billion by 2025 with a 17.8% CAGR in line with the global battery demand.

On the other side, the square meters of material used could double from 8,191 (MM sm) in 2022 to 15,877 (MM sm) in 2025.

MMAT Investor Presentation Nov 2022

The second technology developed by Meta concerns the collectors used in batteries. The product is called PLASMAFusion and aims to reduce the weight of the copper used in the collectors by about 80%, increasing the duration of the charge and the safety of the battery. This second technology therefore also affects the efficiency and cost of the final product.

Related to this kind of technology the Company underlines also an agreement (memorandum of understanding -MOU) with two big market players (last earnings call):

we announced this beautiful MOU with 2 exciting companies, one of which is Mitsubishi Electric. The other one is DuPont. And Together, we are trying to scale this technology to also address the next generation of batteries, solid-state batteries, where the coating process is one of the key areas of innovation.

Also about this new disruptive technology, MMAT is moving on the market and has begun important relationships to set up the development and marketing of the product.

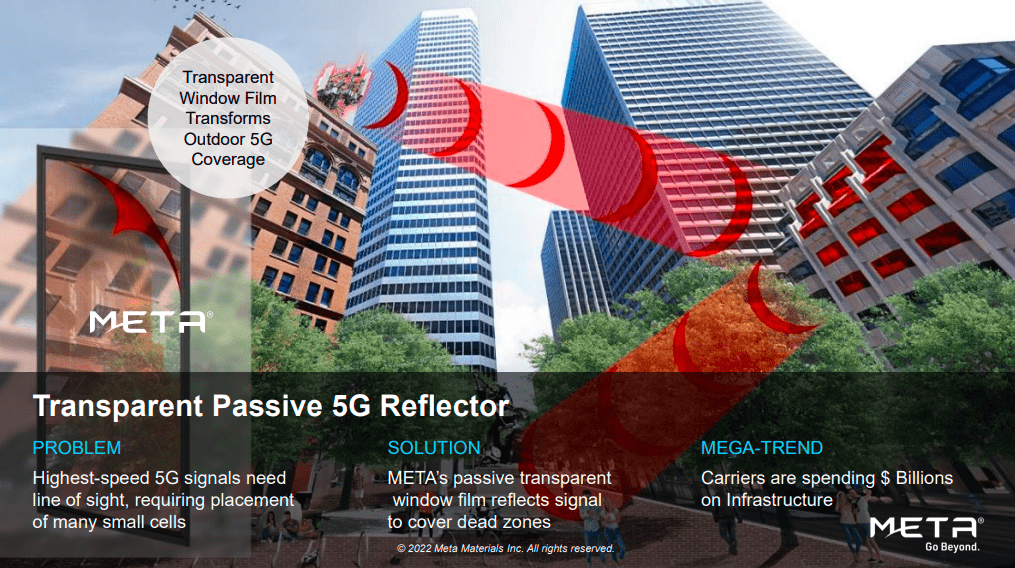

ADAS (advanced driver assistance systems) and 5G

ADAS is a highly technological device that enables autonomous driving of vehicles using antennas, sensors, and radars. All these devices work correctly if they are not affected by atmospheric agents such as rain, snow, or fog. MMAT, through its lithographic products, can solve all these problems and enable the correct functioning of the devices in any weather condition.

Concerning the market and its growth, as seen in the previous paragraph, we can hypothesize a double-digit rate and therefore the potential of this new technology is very high.

The is expected to grow from$1.99B in 2022 to $131.4B in 2030 and this represents a further element of strong interest on the part of all service providers.

MMAT Investor Presentation Nov 2022

MMAT is positioned on the market with a transparent film that can be placed on the windows of buildings and can reflect the 5G signal in all the neighboring dead zones which would require an ‘ad hoc’ installation of special antennas.

Many risks and why to sell

Revenue Instability

Most of the revenue is generated thanks to the development and engineering of the product and this creates the impossibility of making a reliable forecast in the medium term. For example, Q3-22 revenue was lower than Q1 and Q2 and Q3 revenue was mainly generated by the development of nano-optic technology for banknotes. In any case, if we look at the 2020 Revenue of $1.12M and compare it with 2022 (TTM) of $11.1M, the figure has increased tenfold in just 2 years but, at the moment, there are no guarantees that this trend will continue in the coming quarters.

The only element of greater certainty is represented by the Frame Agreement with the development of a security feature for a Central bank ($41.5M in 5 years).

Operational Expenses

The Company is continuing to invest heavily in growth and if we compare Q3-22 vs. Q3-21 operating expenses they doubled from $12M to $23.9M.

How can we listen to the founder in the last earnings call:

We did a number of acquisitions this year that triggered additional spending in the G&A side. And so that’s what you’re seeing in the bumps. And our plan for next year, has that dropping back again to more rational levels. And as you know, there’s some ongoing investigation from the SEC that’s taking legal fees and all of that’s going to drop in the ’23 time frame from a cost standpoint.

Acquisition, SEC investigation, and Headcount represent the main expense factors.

Cash Flow, CapEx, and Funding

Meta currently has $2.9M of single long-term debt and this may not represent an element of high risk. However, if we compare the cash used in Q3 operations equal to $19.5M or that of the first nine months of 2022 which is equal to $48M we can underline that there is a big cash flow problem. In terms of CapEx in Q3 $3M was used and in 2022 (nine months) $11.9M and as the company itself states in the last earnings call:

‘We believe that cash on hand, combined with our projected revenues and expense management capabilities will be sufficient to support our needs for the next 12 months.’

Business survival could be guaranteed for about 12 months and this represents a high element of risk especially if we think that to make further investments for the development of new products it will certainly be necessary to resort to new third-party capital. And this may not be guaranteed.

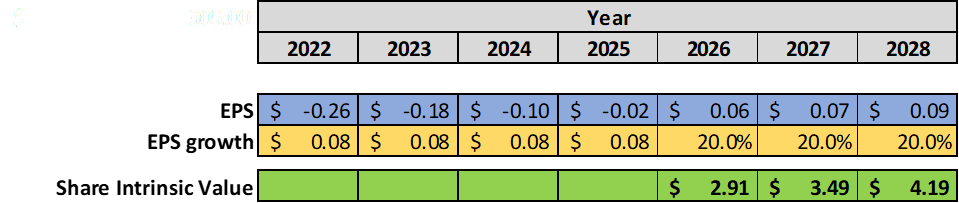

EPS growth model valuation

Since the company is showing growth in terms of Revenue and EPS, I decided to use a formula based on EPS growth assuming that EPS could become positive in 2026 with an annual rate of increase of about $0.08 or the one officially assumed on the estimates for 2023. Starting in 2026, I assumed a 20% annual EPS growth rate.

The Formula is (by popular investor Benjamin Graham):

Intrinsic value per share = EPS x (8.5 + 2 g)

Where

EPS = earnings per share

g = EPS growth rate = $0.08 from 2022 to 2026 and 20% from 2026 to 2028

Author Calculation

Example of calculation for 2028:

Intrinsic value per share = EPS x (8.5 + 2 g) = 0.09x(8.5+2×20) = $4.19

The last intrinsic value of $4.19 for 2028 underlines an annualized return (CAGR) of 25.2% as the current share price is $1.09.

25.2% is the annualized expected return for the investment in MMAT. It’s a very good figure and it requires very high-risk confidence that the EPS can become positive in 2026.

Peer comparison

Meta Materials Inc. is the first Metamaterials Company listed on NASDAQ and for this reason, it is not possible to identify comparable peers in the same business field. The closest business sector could be semiconductors and, on this topic, we could simulate a possible peer comparison. Having said this, I have defined some companies operating in the Semiconductor industry with market capitalization similar to MMAT.

- Magnachip Semiconductor Corporation (MX)

- Valens Semiconductor Ltd. (VLN)

- Transphorm, Inc. (TGAN)

- SkyWater Technology, Inc. (SKYT)

Seeking Alpha

Using the Seeking Alpha Quant Rating we can see how MMAT gets a ‘Hold’ rate which compared with its peers we notice that SKYT gets a ‘Buy’ and could represent a better investment opportunity.

Seeking Alpha

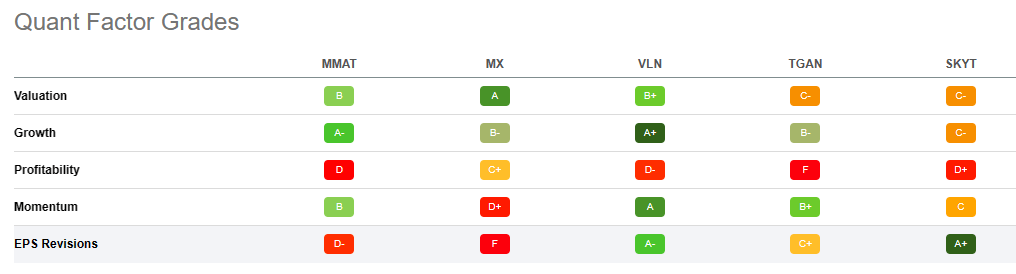

Going into the details of the evaluation components we can see, on the one hand, how MMAT has no better element than its peers while on the other hand, it has no worse ratings than its peers. It is placed in a middle position.

Wishing to draw a conclusion we can say that from an investment point of view in the semiconductor market there are perhaps better alternatives but if we want to bet on metamaterials, MMAT represents the only real alternative listed on the Nasdaq.

Conclusion

Meta Materials Inc. represents a company in the early stages of business development. Revenue is growing significantly but there are no certainties about its stability in the following quarters. The products (in terms of metamaterials) are highly innovative and cover rapidly expanding market sectors (EV and 5G above all). This represents a very positive and functional element for the company’s growth. On the other hand, the fundamentals are very poor in terms of profitability and cash flow and it may take a long time to see positive results. With strong assumptions, the evaluation of the share price is attractive but the business’s intrinsic risks require, in my opinion, more confirmation. My rating is on Hold.